We’ve just marked 2 years since PSD2 went into full power across Europe and in the UK, on September 14, 2019. This was a good occasion for us to reflect upon how far open banking has come and what has to be improved so that it gets widely adopted.

Salt Edge has thoroughly analysed the performance of 2500 PSD2 APIs in 31 European countries, and the overall open banking journey they offer – both to third parties and end-customers, and compiled the identified results into a report: “State of open banking payments in Europe in 2021”.

One might expect more things to have been achieved in these 2 years, yet we identified interesting dynamics compared to 2020. While last year, not all PSD2 bank APIs were working, particularly the payment initiation ones were broken, this year we registered higher availability of APIs and better quality overall, with the top 10 EU countries having rates ranging from 97.61% to 91.12%. This means that the APIs are becoming more reliable now. Also, the launch of EBA Opinion back in June 2020 had a great impact on banks’ implementations, more of them now supporting app2app redirects, while some banks excluded the multiple redirects during user journey.

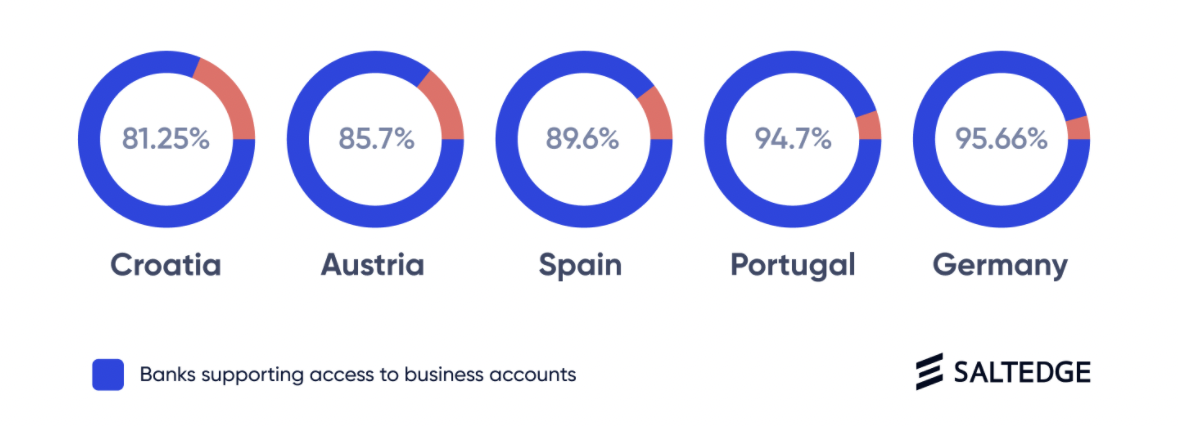

Besides, out of the almost 2500 regulated APIs integrated by Salt Edge across Europe, 72% claim to be supporting access to business accounts. Germany, Portugal, Spain, Austria, and Croatia are the countries with the highest percentage of banks offering access to both personal and business accounts, creating an environment suitable for innovative services to emerge.

I’ve always said that, when done right, the benefits of open banking can be huge, by changing the way people and businesses pay and operate. But the key word here is “done right”. We still stumble upon errors, broken links, late replies from banks, the obligation for the end-user to needlessly share personal data during payments (i.e. beneficiary’s email), unnecessary friction during the user journey, different interpretation of RTS requirements across EU countries—more details can be found in the report. All aforementioned technical and user experience obstacles, accompanied by a poor education of the market, particularly of end-customers, on what open banking is and its benefits, result in low adoption rates.

It is exciting to see all sorts of businesses including lending, accounting, credit bureaus, banks, PFMs, treasury management, PSP and merchants to have understood the payments’ massive opportunities and the power of easy access to bank data afforded by open banking. However, to help end-customers in actually adopting open banking-powered solutions, it is critical both to ensure a smooth and intuitive user journey—where banks play an important role, and to implement a clear and consistent communication strategy. I’ve noticed countries, for example, the Netherlands, where the national regulator takes a more proactive approach and requires ASPSPs to pass an audit check of their PSD2 compliance solution. I hope all national regulators follow this example, and also to further consider imposing sanctions on banks that don’t follow the compliance rules, to get involved in national communication campaigns for consumers’ education, perform regular reviews and metrics collections from both banks and TPPs.

Keeping a collaborative attitude from all sides will help increase the adoption rates exponentially. An efficient cooperation between banks and TPPs with the guidance of regulators will enable open banking to accomplish its initial goal.

Download the report to discover more about the current reality of open banking in Europe, the identified differences between 2020 and 2021, the biggest obstacles in open banking payments, and much more.