Switching to the Satoshi standard and Lightning Network connectivity makes Bitcoin more tangible and easy to use. AAX has made the first move in the crypto space, already providing BTC to SAT

Switching to the Satoshi standard and Lightning Network connectivity makes Bitcoin more tangible and easy to use. AAX has made the first move in the crypto space, already providing BTC to SAT

The Monetary Authority of Singapore (MAS) and Elevandi (a not-for-profit entity set up by the MAS to connect people and businesses, ideas and insights in the FinTech sector in Singapore and globally) today announced the return of the Singapore FinTech

Doconomy, a Swedish world-leading impact tech provider for banks, SMEs, and corporates, joined forces with Salt Edge, a leader in offering open banking solutions,

The Future Blockchain Summit, the MENA region’s longest running exhibition and conference connecting key stakeholders across Blockchain, crypto, and Web 3.0 will return to

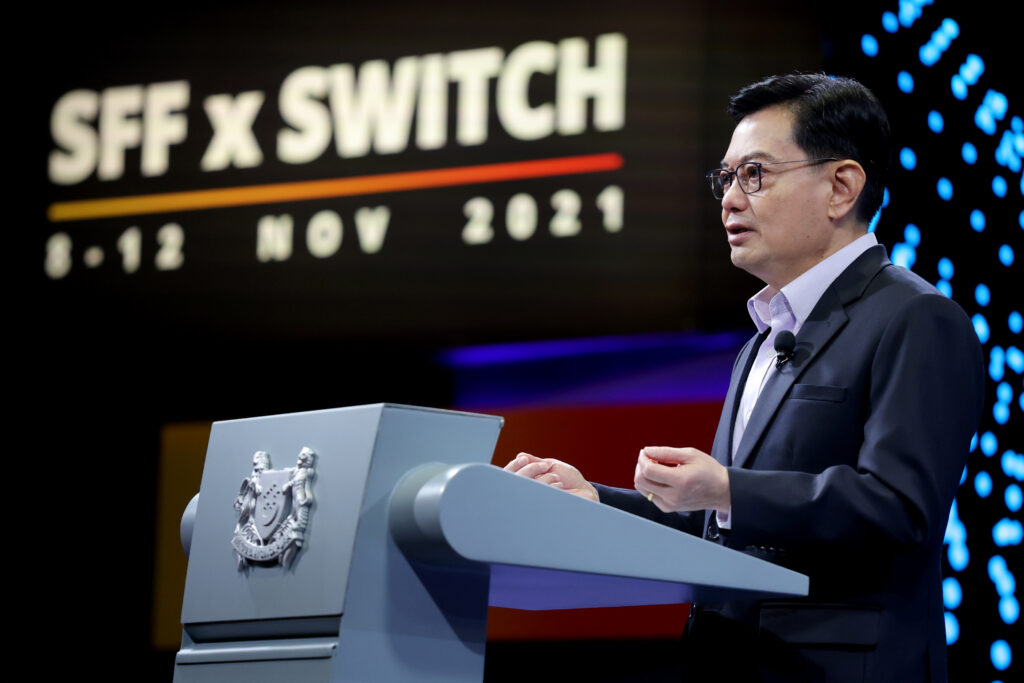

The National Artificial Intelligence (AI) Programme in Finance was launched today at the Singapore FinTech Festival x Singapore Week of Innovation and TeChnology (SFF x SWITCH) 2021 by Mr Heng Swee Keat, Deputy Prime Minister.

The Programme is a joint initiative by the Monetary Authority of Singapore (MAS) and the National AI Office (NAIO) at the Smart Nation and Digital Government Office (SNDGO). It aims to build deep AI capabilities within Singapore’s financial sector to strengthen customer service, risk management, and business competitiveness.

The Programme is part of Singapore’s broader National AI Strategy1 and seeks to enhance the ability of financial institutions (FIs) to research, develop and deploy AI solutions. I

The Programme currently comprises various initiatives – Initiative Description NovA! – an AI technical platform to generate insights on financial risk. In the initial phase, NovA! will help FIs harness AI to assess companies’ environmental impact and identify emerging environmental risks.

NovA! will be developed by Aicadium, a Temasek portfolio company, other local FinTech firms and Singapore-based banks, and will include additional use cases in subsequent phases.

Launched in 2019, the National AI Strategy aims to establish Singapore as a leader in developing and deploying scalable, impactful AI solutions, in key sectors of high value and relevance to our citizens and businesses by 2030. National AI Projects were renamed National AI Programmes to better reflect the scope of work under the initiative. Veritas An AI governance initiative to help FIs utilise AI and Data Analytics (AIDA) responsibly based on MAS’ fairness, ethics, accountability, and transparency (FEAT) principles. The initiative includes developing the Veritas Assessment Methodology and Veritas Toolkits, and the Veritas Ecosystem, Anti-Money Laundering / Countering Financing of Terrorism (AML/CFT) Surveillance and Analytics Programme (ASAP) A programme which focuses on enhancing analytics for AML/CFT surveillance.

One key initiative is COSMIC (Collaborative Sharing of Money Laundering/Terrorism Financing Information and Cases) to be rolled out in 2023. The secure data sharing platform enables FIs to share and analyse information on customers or transactions that cross material risk thresholds. Such information will help FIs identify and disrupt illicit networks, and safeguard Singapore as a financial centre.

The National AI Programme in Finance will create good jobs for citizens and commercial opportunities for businesses.

An integrated, seamlessly connected financial platform and FinTech talent are vital to the development of the Greater Bay Area (“GBA”), says Jessica Tan, co-CEO of Ping An Group. The GBA is a huge and exciting area. Ping An, together with its associate company OneConnect is always willing to use technology as an enabler for the GBA’s digital economy, she said. OneConnect Financial Technology Co., Ltd. (short for “OneConnect “,NYSE: OCFT) is a leading technology-as-a-service platform provider.

Ms. Tan underscored the importance of cultivating Hong Kong’s FinTech capabilities in a keynote delivered at Hong Kong FinTech Week. Held from November 1-5, this year’s event gathered world-renowned speakers, regulators, and industry players to “scale the FinTech future together.”

“Building a seamless digital economy is the greatest opportunity in the region. But practically, we must address three key issues in order to capture and maximize that opportunity. This is not something that an individual entity or organization can solve — it requires a collective effort across the entire GBA. This is where Hong Kong, the region’s international finance hub, can take the lead and harness technology to make FinTech platforms more interoperable,” said Ms. Tan.

Building a shared digital economy across the GBA

With Hong Kong’s financial expertise, Guangzhou’s manufacturing prowess and Shenzhen’s technological capabilities, the GBA is the perfect region to develop a world-leading digital economy. However, the region will need to address key challenges surrounding governance and regulation, Small and Medium-Size Enterprises (SMEs) support, and local talent if it wants to transform these opportunities into a reality, said Ms. Tan.

The GBA involves three different jurisdictions, each with its own government authorities, standards, and procedures. All these need to be considered when developing a connected financial platform, said Ms. Tan. At the same time, regulators and organizations need to be clear on how financial services can empower SMEs with the access and capabilities to operate seamlessly across regions, particularly given half of all trade in the GBA is conducted by small businesses. Lastly, Hong Kong needs to find and nurture the right talents to fuel innovation and development.

Technology as an enabler for the GBA’s digital economy

According to Ms. Tan, technology is essential to resolving these issues and making platforms truly interoperable across the GBA. Notably, Hong Kong should seek to consolidate its various government data and services, similar to the one-stop sandbox platform proposed by regulatory authorities to enable GBA start-ups to develop cross-border fintech tools. At the same time, data should be available across regions to ensure that various jurisdictions and government entities adhere to the same standards — all while delivering a seamless experience to clients and companies.

OneConnect has already established such a platform to empower all enterprises, including SMEs, to participate in, and prosper from, the digital economy. Earlier this year, the company celebrated the first anniversary of Ping An OneConnect Bank (“PAOB”), the first virtual bank in Hong Kong to use alternative data models for risk assessment. PAOB uses trade data and other information to assess and predict risk in order to provide non-collateralized loans for SMEs. To date, PAOB has served HK local SMEs with total assets reaching HK$1 billion.

OneConnect has also established the Guangdong-Hong Kong-Macao Greater Bay Area Port Logistics and Trade Facilitation Blockchain Platform to facilitate cross-border trade between merchants, and the Guangdong SME financing platform to improve lending efficiency for SMEs.

In addition to building the right platforms, OneConnect is nurturing the talents of tomorrow and bridging skillset gaps across the region. Its new internship program connects aspiring professionals with established financial services and technology experts to encourage knowledge transfer.

Furthermore, its parent company, Ping An Group has launched an incubator accelerator program for the GBA. The program plugs up-and-coming companies into an open Fintech platform that serves existing financial services, companies and corporations — in turn encouraging and growing entrepreneurs within the region.

“The GBA is a huge and exciting area with plenty of opportunities. But we can only take advantage of these opportunities with a collective effort that gives full play to Hong Kong’s position as an international financial center. By using technology to bring financial institutions, FinTech companies and people together, we can promote greater cross-border collaboration and turn this vision into a reality,” said Ms. Tan.

By 2030, 60% of global consumers will have made a transaction using a unit of value other than fiat currency, while 73% of global consumer payments will be processed by non-financial institutions on the Internet of Payments.

Revealed on the first day of the Singapore FinTech Festival 2021, these forecasts by market research firm IDC reinforce the need for incumbent financial institutions to adapt their technology quickly for a market in which consumers expect more choice in terms of units of value – including digital assets and loyalty program points – as well as more tailored payments and credit propositions.

They also spell out the cost of failing to adapt: US$250 billion of payments revenue could otherwise move to non-financial institutions by 2030, according to IDC estimates.

“The payments industry is undergoing a massive transformation: non-cash payment volumes are soaring, on-demand payments are gaining traction, and cloud computing and new technology have unleashed a wave of innovation, such as BNPL,” said John Mitchell, CEO of Episode Six. “This is creating a more level playing field for new entrants, and significant challenges for incumbents. The research we’ve unveiled today shows why financial institutions need technology that transfers any unit of value, as well as designed to be configurable and easily integrated into existing financial ecosystems, allowing our clients to bridge the old with new.”

“Financial institutions and non-financial institutions are both vying for a key role in the ownership of payments,” said Cyrus Daruwala, Managing Director IDC Financial Services & FinTech. “IDC forecasts that by 2030, 73% of consumer payments will be handled by non-FSIs through the Internet of Payments. Yet, FSIs are far from out of the payments game – they need to reshape the role they can play in payments of the future and the next-gen payments

technology to succeed.”

IDC’s data shows that 73% of financial institutions around the world have technology infrastructures for payments that are ill-equipped to handle payments for 2021 and beyond. For many incumbents, that means existing payments infrastructure needs to be upgraded payment workflows need to be more data-driven, and risk management needs to be more flexible to adapt to the regulatory requirements for non-fiat currencies and other units of value.

Legacy tech holds banks back yet legacy technology is costing financial institutions more and more, restricting investment in vital digital transformation. IDC estimates that financial institutions’ global spending on payments technology will double from US$39.7 billion in 2020 to US$80.3 billion in 2030.

“Banks need to embrace the new types of payments that recognize that value comes in many forms, but they have a lot of work in front of them,” added Episode Six’s Mitchell. “There are infrastructure and process bottlenecks, resources are being drained on maintaining outdated and disparate systems, and siloed thinking is preventing innovation. Risk aversion can also lead to lost opportunities.”

With the rise of embedded finance, and Banking as a Service solutions, non-financial players can offer payments solutions and are increasingly owning the customer relationship. By 2030, IDC forecasts that 74% of digital consumer payments globally will be conducted via platforms owned by non-financial institutions.

Although banks will no longer dominate payments as they have in the past, this does not mean they may be sidelined altogether. Instead, they need to rethink how they interact with fintech, as well as the new generation of blockchain-based digital finance, provides, said Mitchell at Episode Six.

“Users demand the unified and polished interfaces and smart data-driven products offered by fintech,” he argued. “Economies need the stability and consumer protection that exist when regulated institutions provide financial services, drawing on their long-standing strengths in risk management and compliance. For banks and fintech, the choice, with a few exceptions, will ultimately be to converge or crumble.”

Commonwealth Bank of Australia will become the country’s first to offer retail clients crypto services, Australia’s largest bank said on Wednesday, marking a change from the sector that had refused to do business with cryptocurrency providers.

Starting with a pilot this year, Commonwealth Bank will partner with Gemini Trust Company LLC, a New York-based crypto exchange, to offer trading in 10 cryptocurrencies through its banking app, which is used by about 6.4 million customers.

Commonwealth Bank of Australia will become the country’s first to offer retail clients crypto services, Australia’s largest bank said on Wednesday, marking a change from the sector that had refused to do business with cryptocurrency providers.

Starting with a pilot this year, Commonwealth Bank will partner with Gemini Trust Company LLC, a New York-based crypto exchange, to offer trading in 10 cryptocurrencies through its banking app, which is used by about 6.4 million customers.

At the time, Comyn said CBA was studying the space but had also previously cancelled some business accounts of customers who were doing business with cryptocurrencies.

CBA said its decision to offer the service had been driven by growing client demand for digital currencies and follows other fintech offering crypto services such as Square, PayPal Holdings (PYPL.O) and British-based Revolut.

DBS Bank, a leading financial services group headquartered and listed in Singapore with a presence in 18 markets, has joined the Hedera Governing Council, the group of diverse organizations responsible for stewarding the Hedera network – the most used, sustainable, enterprise-grade public network for the decentralized economy. The Hedera Governing Council comprises heavyweights in the technology, corporate, non-profit and academic arenas.

As the first and only bank in Southeast Asia to join the Governing Council, DBS will explore further opportunities and potential use cases to leverage the vast potential of blockchain and distributed ledger technologies as it continues to reimagine the future of banking.

DBS has been actively leveraging blockchain to offer solutions in areas including cross-border payments and settlements as well as trade financing. With asset digitalisation and tokenisation fast gaining traction, DBS also launched its blockchain-backed digital asset ecosystem last year. Anchored by the DBS Digital Exchange, DBS is able to offer corporate clients and accredited investors an integrated suite of solutions across the digital asset value chain

Jimmy Ng, Group Chief Information Officer and Head of Technology & Operations at DBS, said, “DBS is pleased to join some of the world’s most established organisations on the Hedera Governing Council as we collectively seek to uncover the vast potential of blockchain and distributed ledger technologies. We have been leveraging emerging technologies to reshape the future of banking and have in recent months brought to market a number of innovative offerings powered by blockchain to help our clients seize opportunities in the new normal. We look forward to joining our peers on the Hedera Governing Council in exploring further use cases that bring tangible benefits to our stakeholders.”

“We are pleased to bring this relationship to fruition and have DBS join the Hedera Governing Council,” said Mance Harmon, CEO of Hedera Hashgraph. “In our discussions over the last few years, it has been clear that they are a leader in both the management and in building an ecosystem for digital assets, as well as in emerging adoption of blockchain and DLT to drive efficiencies across their entire business. We look forward to collaborating with them and the other council members, themselves leaders in the finance, payments, legal, and technology arenas, to continue our mission for the Hedera network to serve as the trust layer of the internet.”

Enjin, the leading ecosystem for NFTs, today opens nominations for the second annual NFT Awards. Running from today until November 26th, nominations and community voting for the NFT Awards are now open on nftawards.org. The second edition of the program will celebrate the Metaverse, honoring projects that are driving the future of human experiences through NFTs. The awards ceremony will take place on January 12th, 2022 in Decentraland.

Witek Radomski, Co-founder & CTO of Enjin and NFT Awards judge, said, “We established the annual NFT Awards to commend innovation in our industry, and we look forward to recognizing the incredible progress made within the Metaverse. Following a standout year for the NFT space, this community-driven event will feature and celebrate the world’s most influential NFT projects, and we invite all creators and collectors to submit your favorite projects for consideration today.”

Nominees of the NFT Awards will be determined entirely by community submissions and voting, with the top ten public votes in select categories gaining a spot before an expert judging panel. The confirmed list of judges includes:

Nominations can be submitted on nftawards.org for 10 awards categories, including: Best Avatar; Best Collaboration; Game of the Year; Best Digital Fashion; VR/AR; Best Virtual World; Newcomer Game; Utility; Most Innovative Art; and Project of the Year.

The event will feature members from every corner of the crypto sphere, from NFT creators and game developers, to leading crypto organizations and metaverse projects. The program will be supported by Enjin’s partners VentureBeat, Crypto.com, Decentraland, Rarible, CoinMarketCap, the Blockchain Game Alliance, DappRadar and Product Hunt.

Micah Johnson, whose work ˈsä-v(ə-)rən-tē won 2020 NFT of the Year, concluded: “The same year I won NFT of the Year, I was carrying my paintings in the rain to a local bar and carrying them home when none of them sold. NFTs have empowered me to spread my message thanks to the support of collectors who believed in me, and the NFT Awards program is providing a venue to recognize and elevate the work of fellow creators in the NFT community.”

Please visit nftawards.org to nominate or vote for the NFT Awards, or get in touch at nftawards.org/contact if you believe you fit the criteria for the expert judging panel.

Nigeria on Monday became the first African nation to launch a digital currency – the eNaira – a move its leaders said will expand access to banking, enable more remittances and even grow the economy by billions of dollars.

Africa’s most populous nation joins the Bahamas, the first to launch a general-purpose central bank digital currency, known as the Sand Dollar, in October. China has ongoing trials and Switzerland and the Bank of France have announced Europe’s first cross-border experiment.

But experts and cryptocurrency users in the continent’s biggest economy say the fact that there are more questions than answers regarding the eNaira – and a large amount of worry over the consistency of Central Bank (CBN) rules – means the government faces a tough path to make the eNaira a success.

Central Bank Governor Godwin Emefiele said during Monday’s launch that there had been “overwhelming interest and encouraging response”, adding that 33 banks, 2,000 customers and 120 merchants had already registered successfully with the platform, which is available via an app on Apple and Android.

Some 200 million nairas’ worth of eNaira, which will maintain parity with the traditional currency, has been issued to financial institutions, he said. President Muhammadu Buhari said use of the currency could grow the economy by $29 billion over ten years, enable direct government welfare payments and even increase the tax base.

Nigeria’s young, tech-savvy population has eagerly adopted digital currencies. Cryptocurrency use has grown quickly despite a Central Bank ban in February on banks and financial institutions dealing in or facilitating transactions in them.

Nigeria ranked seventh in the 2021 Global Crypto Adoption Index compiled by research firm Chainalysis.

EQIFI, the decentralized finance (DeFi) platform for lending, borrowing, and investing for ETH, stablecoins, and select fiat currencies, has announced the launch of its global, secure, crypto Mastercards. These debit cards allow users of the platform to make real-time payments in-store and online leveraging digital assets. EQIFI is backed by EQIBank, the wealthtech innovator and the regulated, borderless digital bank for crypto and traditional assets, giving users of the DeFi platform access to a range of banking products and services.

Brad Yasar, CEO of EQIFI, said: “We are tremendously excited to bring EQIFI’s debit cards to our current and future users. This is a major step towards combining the benefits of DeFi with mainstream, traditional banking and payments processes. Having a physical, tangible product that our users can incorporate into their everyday lives illustrates how DeFi is steadily revolutionising financial practices. By combining DeFi, crypto, and traditional payment rails the future of finance is well and truly here.”

Accepted in over 44 million locations worldwide and capable of processing international online and offline payments, the EQIFI Mastercard is secured with an EMV chip and PIN capabilities to prevent fraudulent spending. The EQIFI Mastercard has some of the highest limits in the industry, and boasts zero spending limits, allowing users to apply their DeFi assets to spend freely in the real economy. Verified users who stake EQX tokens will have priority access to obtaining their EQIFI Mastercard. To ensure the highest security standards and regulatory compliance, users must complete Know-Your-Customer (KYC) verification before receiving their debit cards.

Currently, payments made via EQIFI debit cards convert assets to fiat at the point of sale. Following this initial launch, EQIFI plans to develop an automated process where crypto is directly spent via the debit cards, facilitating payment through digital assets including Bitcoin, Ethereum, and other ERC-20 tokens.

EQIFI recently partnered with industry titan Tezos to launch its suite of decentralized financial products, which includes fixed- and variable-rate lending products, as well as the advanced yield aggregator and interest rate swaps. As a leading Proof-of-Stake (PoS) network with time-tested on-chain governance, an active DeFi ecosystem, and a global community of builders and creators, Tezos was carefully selected to facilitate EQIFI’s continued growth and flagship launch.

Jason Blick, CEO of EQIBank and Chairman of EQIFI, said: “The partnership between EQIBank and EQIFI was designed to bridge the gap between DeFi and traditional finance. We understand that our clients want regulated access to digital assets. That’s why we’re excited to launch the EQIFI Mastercard to give EQIFI users access to a full range of innovative DeFi based banking products and services. The launch of EQIFI’s debit cards is an integral step and milestone in the mission to increase the financial freedom of our many customers, allowing them to integrate digital assets into their everyday lives.”

Money Minx, a US-based net worth and investments tracking platform, joined forces with Salt Edge, open banking pioneer, to allow their users in the UK, Germany, and Switzerland to connect all bank accounts and monitor investments with ease – all in one place.

The modern world opens the door for innovation in major parts of people’s lives, and investment is not an exception. Digitalisation creates many new forms of investment, making them affordable and easier for almost every member of today’s society. Investors look for instant and transparent access to financial planning and portfolio management tools to control, track, and compare investments — in real-time. Here Money Minx enters the arena, offering a DIY investing experience with full control over assets, debt and investments from around the world and in any currency. Combined with Salt Edge data aggregation and data enrichment tools, Money Minx expands the boundaries and takes investing to an entirely new, game-changing level.

The collaboration with Salt Edge helps Money Minx to build a “Personal Finance Mission Control” for the everyday investor by implementing PSD2 compliant access to clients’ bank data across Europe. Open banking-enabled live bank feeds offer an easy way to track investments from anywhere and in any currency — all in one simple, user-friendly place. By teaming up with Salt Edge, Money Minx can cover 50 countries globally by integrating with only 1 API instead of having to connect with each financial institution on its own. Salt Edge solutions enable users to connect their bank accounts in Europe to Money Minx in just several clicks. The entire process is automated, eliminating the need to download statements and enter values in Money Minx manually.

When we were searching for a partner we wanted to make sure our users’ data would be secure. Salt Edge turned out to be more established and transparent than its competitors, so our choice was clear. Currently, we are live with Salt Edge in the UK, Germany, and Switzerland. Very soon we plan on opening connections in Australia, France, Spain, and Italy. We believe our approach to investing makes us stand out against the competition and with such a reliable partner and at our side, we have a very bright future ahead.

Hussein Yahfoufi, Co-founder of Money Minx

We are constantly pushing the envelope, aiming to partner with companies which shape the future of financial services. Modern investing is booming, and innovative businesses such as Money Minx are embracing the benefits of open banking solutions to differentiate and create easy and secure investing experience for their customers.

Vasile Valcov, VP at Salt Edge

PB Fintech FZ (‘Policybazaar UAE’), an online financial aggregator has entered into a technical/API integration with Al Etihad Credit Bureau (AECB) to implement real-time eligibility checks for credit card applications based on the AECB Credit Score and banks’ approval criteria. Customers of Policybazaar UAE can now apply for credit cards having an immediate indication of the chance of their application to be pre-approved based on their AECB Credit Score, which will be pulled automatically by the system. This pre-eligibility check will help enable banks to approve the application faster. Policybazaar.ae will bear the costs of the AECB Credit Score, which will be displayed real-time on-screen and delivered to the applicants via email by AECB.

Marwan Ahmad Lutfi, CEO of AECB said: “This new access channel will make our credit scores easily accessible by individuals through multiple digital distribution channels. Our system now allows marketplaces, aggregators, and potentially any digital platform to integrate with AECB’s systems through APIs. This will enable individuals in the UAE to obtain their AECB Credit Scores through digital channels thereby facilitating access to credit information and making the credit score an integral part of business practice.”

Neeraj Gupta, CEO, Policybazaar UAE said: “This integration will offer our customers an instant and convenient access to their AECB credit scores on Policybazaar.ae platform. This integration lays out an analytical framework for customers in UAE to make informed financial decisions while having immediate access to their financial information. After knowing their actual credit history, customers can create different credit scenarios by evaluating themselves before making the leap towards their next purchase.”

“We advise maintaining a good credit history, which will avoid a higher rate of interest/credit refusals from the lenders and let customers avail of other benefits,” he added.

The AECB Credit Score is a three-digit number that indicates how likely customers are to make their payment obligations on time based on past payment behaviour, which in essence identifies an individual’s creditworthiness. AECB calculates the Credit Score using the information it regularly collects from financial and non-financial institutions in the UAE. The AECB Credit Scores range between 300-900, with a higher score meaning a lower level of risk. For instance, if a customer’s score is 300, it means they are defaulting on a payment such as a mobile phone bill, a loan instalment or even a credit card payment. On the other hand, a good and high AECB credit score (657 or above is considered low risk, or 4 out of five stars), means that a customer’s credit behaviour reflects a lower risk – which translates into easier availability of credit cards and faster loan approvals.

Customer behaviour towards their payment obligations is the main contributor in calculating the AECB Credit Score. To improve Credit Scores and Reports, make payments on time, avoid bounced cheques, reduce unnecessary debt, and reduce outstanding balances on credit cards.